Industry pressure

Why Credit Reporting and Dispute Handling Operations Are Changing

Credit Reporting and Dispute Handling Pressure Is Becoming More Connected

FCRA litigation pressure, dispute abuse, and AI adoption are changing the operating environment for credit reporting and dispute handling teams. At CDIA Connect 2026, industry discussions reinforced that individual FCRA lawsuits are outpacing class actions, disputes are becoming more connected to fraud and risk controls, and AI adoption is moving closer to operational reality.

Recent Q1 2026 developments also show that credit reporting and dispute pressure is not limited to lawsuit counts. Complaint-routing changes, FDIC complaint data, FTC attention, state activity, and continuing litigation pressure are all contributing to a broader environment where dispute handling, documentation quality, and furnishing accuracy need closer operational oversight.

That pressure is not limited to legal teams. It affects how furnishing, dispute, fraud, compliance, and operations teams investigate issues, document decisions, identify recurring data-quality problems, and support reasonable dispute outcomes.

- FCRA litigation pressure continues to rise.

- Individual lawsuits are increasing the importance of early issue resolution and documentation quality.

- Dispute abuse is becoming a fraud, risk, legal, and compliance control challenge.

- AI-generated submissions, online credit repair tactics, and repeated dispute activity are increasing review complexity.

- Complaint-routing changes and agency activity may shift more strain upstream into CRA disputes, direct disputes, evidence handling, and response quality.

- Teams need better visibility across furnishing accuracy, dispute evidence, response quality, and recurring issue patterns.

The practical question is whether teams can identify what changed, review the right evidence, document the basis for the response, and escalate recurring issues before they become complaints, repeat disputes, or litigation exposure.

Litigation

FCRA Litigation Pressure

Q1 2026 reporting showed FCRA case activity remained elevated, with year-to-date filings through March 2026 up 45% compared with the same period in 2025. For furnishers, consumer reporting agencies, lenders, servicers, and dispute teams, litigation readiness starts before a lawsuit is filed. It begins with investigation quality, documentation clarity, and the ability to show that the organization followed a reasonable and consistent process.

Fraud and risk

Dispute Abuse and Fraud Risk

Disputes are increasingly connected to fraud, risk, identity-theft-related claims, credit washing, repeated submissions, and coordinated or internet-influenced tactics. Dispute handling can no longer be treated only as a response process. It is part of a broader fraud, risk, legal, and compliance control environment.

Regulatory visibility

Complaint and Regulatory Visibility

Complaint and regulatory pressure continue to matter, but they should not be viewed in isolation. Q1 2026 developments showed that complaint-routing changes, FDIC complaint data, FTC attention, and state-level activity are all part of the broader consumer-reporting environment.

AI-driven volume

AI-Generated Noise

Generative AI, social media advice, credit repair tactics, and automated submissions are increasing the volume and complexity of dispute materials that teams must review. Teams need to separate legitimate consumer issues from repeated, low-quality, or automation-driven submissions while still supporting reasonable investigations and documented responses.

Related Bridgeforce analysis:

CDIA Connect 2026 insights;

FCRA litigation trends entering 2026;

Q1 2026 social media and AI credit repair trends.

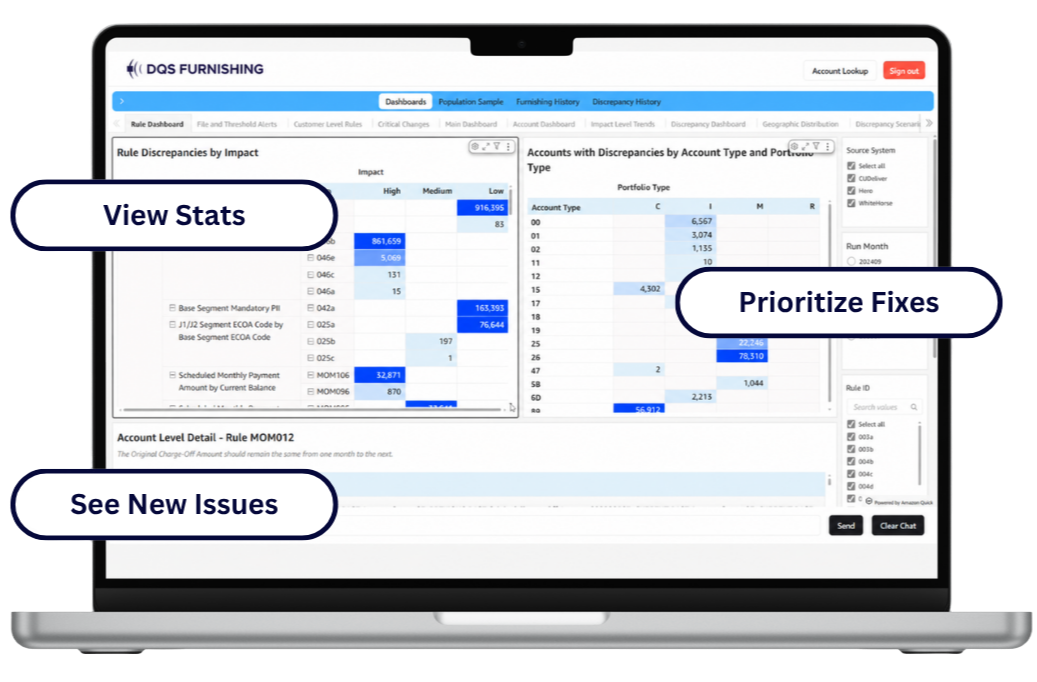

The Core Problem for Furnishing and Dispute Teams

The issue is not only more volume. Furnishing and dispute teams need to identify what changed, what is driving the issue, where risk is concentrated, and what should be reviewed first.

1

What Changed?

Teams need to isolate the reporting change, affected account population, dispute history, response activity, or documentation issue behind a problem.

2

What Is Driving the Issue?

Teams need clearer visibility into the rules, fields, documents, evidence gaps, prior responses, or repeated patterns behind the issue.

3

What Should Be Reviewed First?

Managers need to see where risk is concentrated so review can focus on the highest-impact accounts, populations, unresolved corrections, evidence gaps, or response-quality patterns.

When review tools are too static or difficult to navigate, teams spend too much time finding the problem and not enough time determining what action should be prioritized.

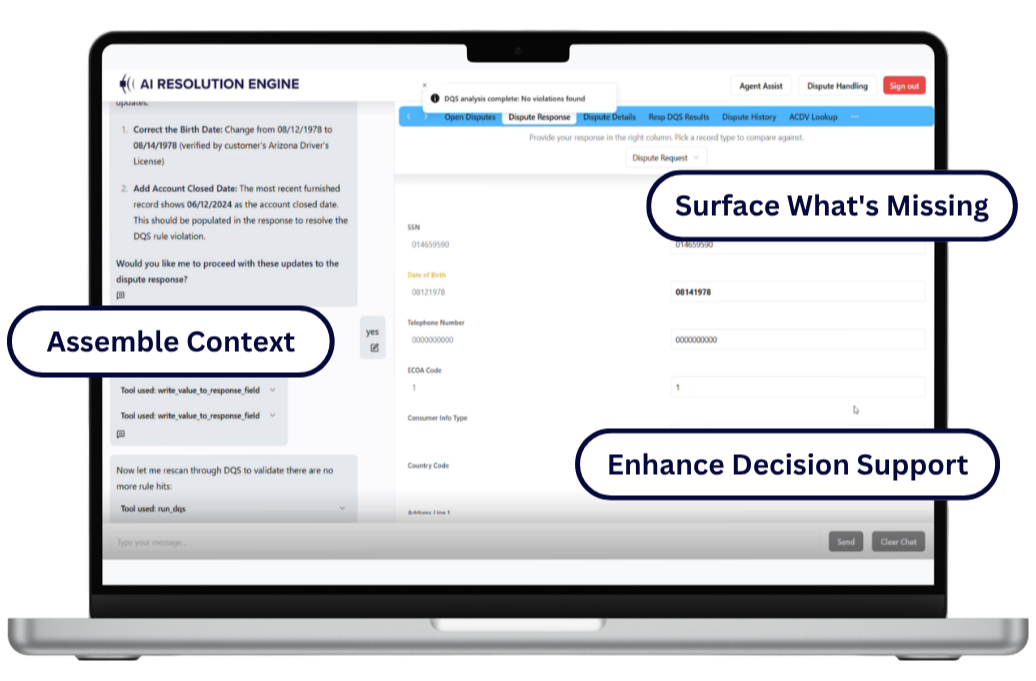

Why Better Investigation Support Is Needed

These pressures do not just create more work. They make it harder for teams to separate recurring data-quality issues, documentation gaps, response-quality problems, and automation-driven noise from the issues that require immediate review.

That matters because getting disputes right early is now a litigation-readiness priority. If a consumer issue can be identified and resolved before it becomes a complaint or lawsuit, the organization may reduce operational burden, legal exposure, and downstream rework.

Better investigation support starts with stronger visibility across furnishing accuracy, dispute response quality, and the patterns that connect upstream reporting issues to downstream disputes.

AI-assisted review can support that goal by helping teams organize complex information, identify patterns, and focus human review where it matters most.